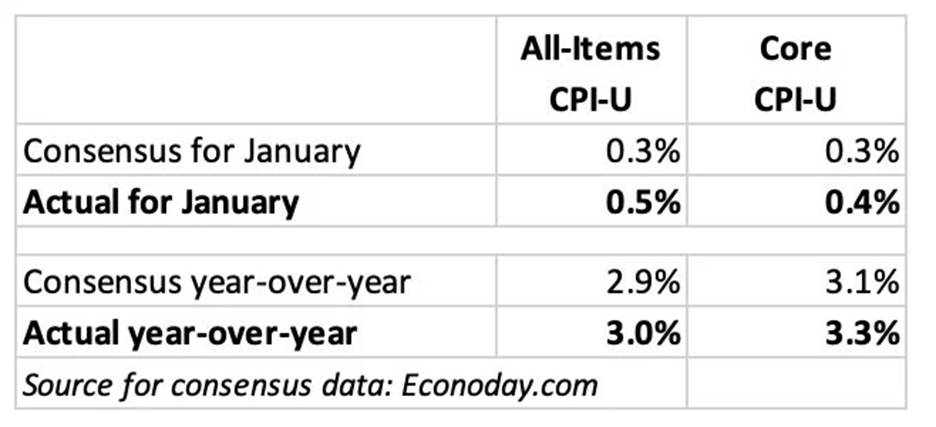

All-items and core inflation both rose much higher than expectations.

By David Enna, Tipswatch.com

The January inflation report, just released by the Bureau of Labor Statistics, demonstrated that U.S. inflation is far from tamed. This was not good news.

There is no silver lining here. Seasonally-adjusted all-items inflation increased 0.5% for the month and 3.0% for the year, both above expectations. Core inflation, which removes food and energy, rose 0.4% for the month and 3.3% for the year, also above expectations. Annual inflation by both measures increased over December levels.

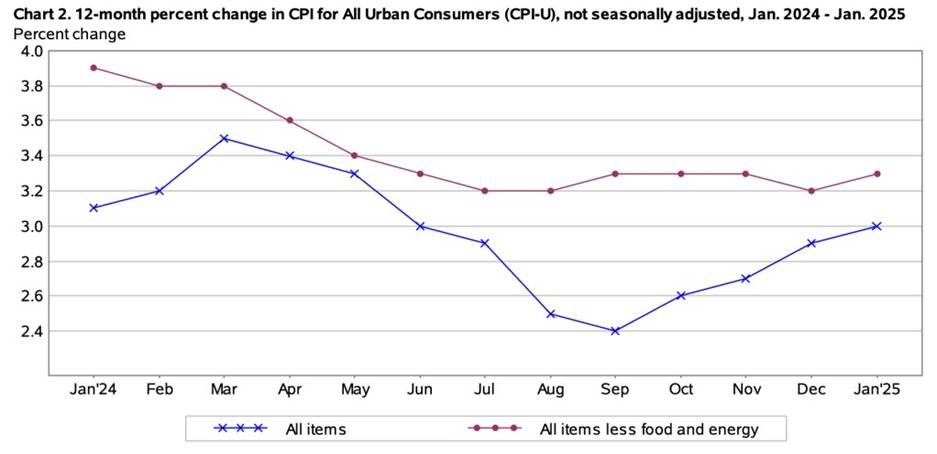

This one graph, tracking the year-over-year trend line, shows it all, with all-items inflation steadily rising higher since fall 2024 and core remaining stubbornly above 3.0%:

The BLS noted that shelter costs increased 0.4% for the month and 4.4% for the year, a major factor in the overall increase. And gasoline prices rose 1.8% for the month, after rising 4.0% in December. Food at home prices increased 0.4% for the month and are now up 2.5% for the year. The price of eggs, for those curious, rose 15.2% for the month. It’s time to switch to breakfast cereal, where prices declined 3.3% for the month.

The BLS said prices were up across all major categories except apparel, which saw costs decline 1.4%.

What this means for TIPS and I Bonds

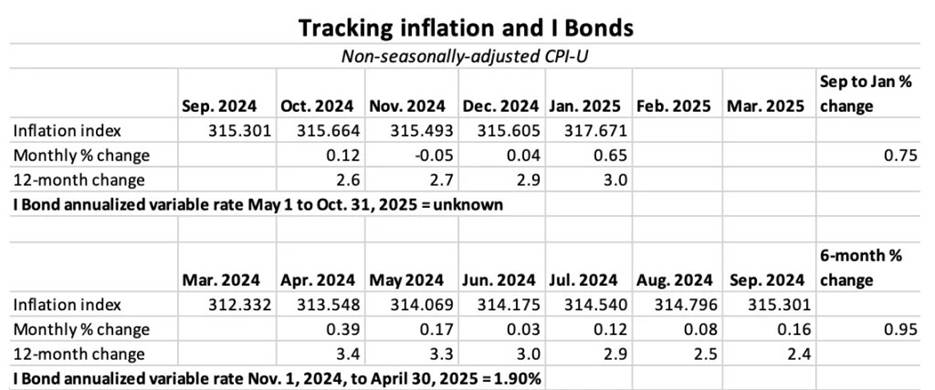

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in nonseasonally adjusted inflation, which adjusts principal on TIPS and sets future interest rates for I Bonds.

The BLS set the January inflation index at 317.671, a sharp increase of 0.65% for the month. A high number was expected, because non-seasonally adjusted inflation runs higher than adjusted inflation from January to June. But 0.65% was higher than I expected.

For TIPS. The January inflation number means that principal balances for all TIPS will increase 0.65% in March, after rising just 0.04% in February. For the year ending in February, principal balances will have increased 3.0%.

For I Bonds. January is the fourth of a six-month string that will determine the I Bond’s new variable rate, which will be reset on May 1 and *eventually roll into effect for all I Bonds. At this point, with two months remaining, inflation has increased 0.75%, which translates to a variable rate of 1.50%. The next two months are likely to push the variable rate up to around 3.0%, or higher. We’ll have to wait and see. Here are the numbers so far:

View historical data on my Inflation and I Bonds page.

What this means for future interest rates

The January surge in inflation (which has been a January trend for several years) supports the Federal Reserve’s decision to hold interest rates at current levels, and probably means no rate-cutting is coming for many months.

*STEELE’S COMMENTARY:

Well then, should your 2025 purchase of I Bonds be made nearly at the end of February ’25 (investing at the end of a month renders return as if invested at the first of the month) or should you wait for the higher reset rate on May 1? The inflation component of an I Bond adjusts every six months – May 1st and November 1st. The inflation component of your I Bond purchase is locked-in for six months after you bought it. While new rates for I Bonds introduced in May and November, your rate changes up or down, every six months from the date of issue. So, if you bought an I Bond in

February ’25 with a composite rate of 3.11 percent (a fixed rate of 1.20% and inflation rate of 1.91%) that return would not change until August, 2025 at which time the inflation component adjustment of April 1st would kick in. Mr. Enna suggests a new inflation rate (“variable rate”) of 3.0 percent or higher, meaning that with a fixed rate of 1.20 percent and a variable rate of 3.0 (maybe more) your composite rate increases to 4.20 percent from 3.11 percent. So, the question becomes: does my two-month purchase deferral of inflation protection, February to April, costing me 0.52 percent, make sense so I can receive 1.50 percent beginning on April 1 instead of September 1? I.e., Should I forgo one-half of 3.0 percent, or 1.5 percent (6 months), to gain 0.52 percent interest in February and March? Doing so means that 1.50 percent becomes 0.98 percent (1.50 minus 0.52 = 0.98). Mathematically, 0.98 of your $10,000 purchase, pro-rated over 12 months, gives you a $196 additional return by delaying until April – perhaps a de minimus result, but value is in the eyes of the beholder! By the way, your purchase limit is $10,000 each calendar year. Buying toward the end of any month renders interest as if you purchased on the 1st of any month. But allow a couple of days for Treasury Direct’s processing of your purchase.

Thoughtfully, for your investment health and well-being, Dan Steele